Managing money across borders is one of the most consequential — and misunderstood — aspects of running a modern business. Whether you’re paying a supplier in Manila, receiving revenue from a client in New York, or managing payroll across multiple territories, understanding the distinction between domestic transfers vs international wires is not optional. It is a strategic imperative.

Many business owners and finance teams treat both as interchangeable. They are not. The rules, costs, timelines, and risks attached to each are fundamentally different — and confusing the two can lead to delayed payments, unexpected fees, and frustrated international partners.

In this guide, we break down everything you need to know: from how each payment type works under the hood, to what it actually costs your business, to how platforms like PhiliPay are redefining what efficient global payments look like for UK businesses operating worldwide.

Table of Contents

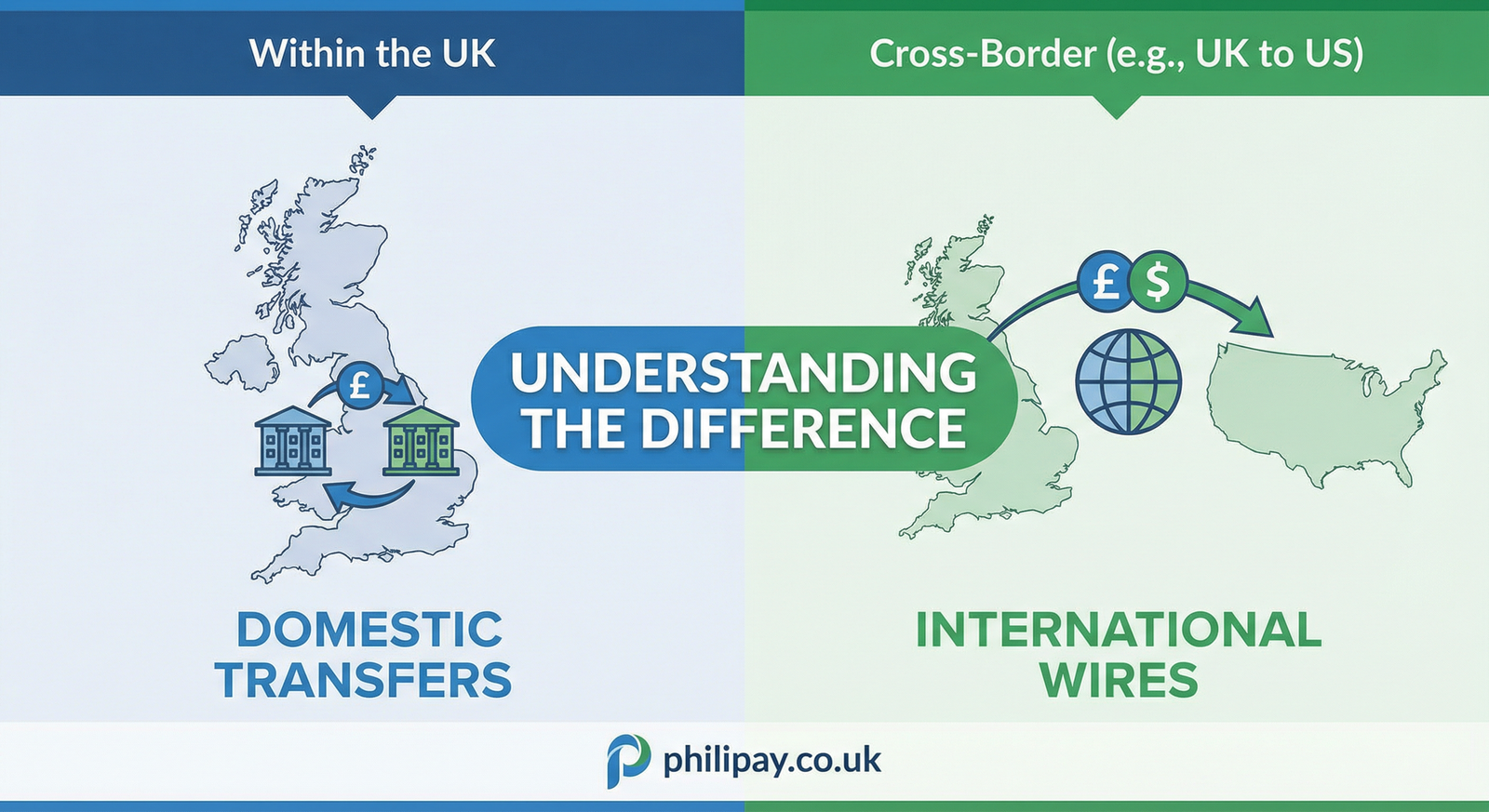

What Is a Domestic Transfer?

A domestic transfer is any movement of funds between two bank accounts that operate within the same country and under the same national payment infrastructure. In the United Kingdom, this means transactions processed through systems such as Faster Payments, CHAPS (Clearing House Automated Payment System), or BACS (Bankers’ Automated Clearing Services).

Each of these systems is designed for speed, simplicity, and low cost within a single regulatory jurisdiction. Faster Payments, for example, can move money between UK bank accounts in seconds — often for free or for a minimal flat fee. CHAPS handles high-value same-day settlements for property transactions or large corporate payments. BACS processes bulk payments like payroll on a two-to-three day cycle.

The defining feature of a domestic transfer is that the currency does not change, the regulatory environment is unified, and the infrastructure is nationally managed. This makes it predictable, fast, and inexpensive.

What Is an International Wire Transfer? {#international-wire}

An international wire transfer — sometimes called a SWIFT transfer — is a payment instruction sent across a global network of correspondent banks to move money from one country to another. SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication, and it is the backbone of cross-border business payments globally.

When your UK business sends a payment to a partner in the Philippines, for instance, your bank does not send the money directly. Instead, it sends a secure message through the SWIFT network, instructing a chain of correspondent banks to debit and credit accounts along the route until the funds reach their destination.

This process introduces layers of complexity:

- Currency conversion at one or multiple points in the chain

- Correspondent bank fees levied by each intermediary institution

- Compliance screening at each node for anti-money laundering (AML) and sanctions checks

- Settlement delays that can range from one to five business days

Unlike domestic transfers, international wire transfers do not operate within a single regulatory framework. They cross jurisdictions, each with their own rules, and this is precisely what makes them more expensive and less predictable.

Domestic Transfers vs International Wires: The 5 Key Differences

Understanding domestic transfers vs international wires comes down to five core dimensions. Each one has direct implications for your business’s cash flow, cost management, and operational efficiency.

1. Speed and Settlement Time

Domestic transfers in the UK via Faster Payments typically settle within seconds to two hours. CHAPS guarantees same-day settlement for high-value transactions submitted before the daily cut-off.

International wire transfers, by contrast, generally take one to five business days to settle. The exact timeframe depends on the destination country, the number of correspondent banks in the chain, time zone differences, and whether the payment triggers any compliance holds. For businesses in time-sensitive industries, this delay is not merely inconvenient — it can be commercially damaging.

2. Cost Structure

This is where the difference becomes most tangible for businesses.

Domestic transfers are typically:

- Free or near-free for standard Faster Payments

- £25–£35 for CHAPS same-day transfers (varies by bank)

- Low and predictable in almost all cases

International wire transfers carry a far more complex fee structure:

- Outgoing transfer fee: Your UK bank may charge £15–£40 per transaction

- Correspondent bank fees: Each intermediary in the chain may deduct a fee (often $10–$30 USD equivalent) from the transferred amount

- Currency conversion spread: Banks typically apply a 2–5% margin above the interbank (mid-market) exchange rate

- Receiving bank fee: The beneficiary’s bank may charge an incoming wire fee

The result? A single international wire transfer can cost your business far more than the headline fee suggests — particularly when recipient countries have additional levies or less liquid currency pairs.

3. Regulatory and Compliance Requirements

Domestic transfers operate under a single national regulatory framework — in the UK, this is overseen by the Financial Conduct Authority (FCA) and the Payment Systems Regulator (PSR). Compliance obligations exist but are streamlined within a unified legal environment.

International wire transfers must comply with the regulations of every jurisdiction the payment passes through. This includes:

- AML and Know Your Customer (KYC) obligations in multiple countries

- OFAC (Office of Foreign Assets Control) sanctions screening for USD-denominated payments

- Beneficiary verification requirements that differ by destination country

- Local central bank reporting requirements (particularly relevant for payments into the Philippines, where Bangko Sentral ng Pilipinas regulations apply)

For UK businesses managing high volumes of cross-border business payments, this compliance complexity is a significant operational burden — and a potential source of delays if documentation is incomplete.

4. Transparency and Traceability

With domestic transfers, both sender and recipient typically have real-time or near-real-time visibility of the transaction status. Most UK banking apps show payments reflected within minutes.

International wire transfers have historically suffered from a transparency gap. Once a payment enters the SWIFT network, tracking it through multiple correspondent banks was — until recently — extremely difficult. Businesses would often have no way of knowing whether a delayed payment was held for compliance review, lost due to an account number error, or simply awaiting settlement at the receiving bank.

This is improving with the rollout of SWIFT gpi (Global Payments Innovation), which now offers end-to-end tracking for wire transfers. However, adoption remains uneven across institutions and geographies.

5. Currency Handling

Domestic transfers are inherently single-currency. A UK domestic payment moves GBP from one account to another — no conversion required, no exchange rate risk.

International wire transfers almost always involve currency conversion, and this is where significant value can be lost. The rate applied by your bank is rarely the mid-market rate you see on Google. The spread between the interbank rate and what your bank charges can be substantial — and on large or frequent payments, this compounds rapidly.

For UK businesses managing global payment solutions, accessing competitive exchange rates and transparent conversion pricing is not a nice-to-have. It is a bottom-line issue.

Hidden Costs Most Businesses Miss

Beyond the headline fees, there are costs embedded in international wire transfers that many businesses fail to account for:

- The mid-market rate gap: Your bank’s FX rate vs. the actual interbank rate can represent a 2–5% hidden tax on every international payment.

- Correspondent bank deductions: These fees are deducted en route from the principal amount, meaning your recipient receives less than you sent — with no prior warning.

- Repair fees: If payment details are incorrect and the wire must be recalled or amended, banks often charge £20–£50+ for the correction.

- Float costs: A five-day settlement window ties up working capital that could be deployed elsewhere.

- Hedging exposure: Without a forward contract or rate lock, businesses are exposed to exchange rate movements during the settlement period.

According to data from the World Bank, the global average cost of sending remittances (a useful proxy for the cost of cross-border payments) remains stubbornly high — you can review their latest findings here: https://www.worldbank.org/en/topic/migrationremittancesdiasporaissues/brief/migration-remittances-data

For businesses processing dozens or hundreds of international payments per month, these hidden costs are not rounding errors — they are material leakage from your P&L.

The Compliance and Regulatory Dimension

Compliance is not merely a bureaucratic hurdle. For businesses operating internationally, it is a genuine risk management function — and mishandling it can result in frozen accounts, rejected payments, or regulatory penalties.

For UK businesses sending international wires, key compliance obligations include:

- KYC on beneficiaries: Particularly for new or high-value recipients

- Purpose of payment declarations: Required by many receiving countries’ central banks

- Source of funds documentation: For large or unusual transfers

- Sanctions screening: Every international payment must be screened against OFAC, UN, and EU sanctions lists

For payments into the Philippines specifically, the Bangko Sentral ng Pilipinas (BSP) has specific requirements around foreign currency inflows for corporate accounts, and beneficiary banks may require additional documentation for large inward transfers.

If your business needs bespoke guidance on the compliance obligations relevant to your payment corridors, speak to the PhiliPay team directly — our specialists understand both the UK regulatory environment and the specific requirements of Southeast Asian markets.

How Multi-Currency Accounts Change the Equation

The traditional binary of “domestic transfer” vs. “international wire” is increasingly being disrupted by the rise of multi-currency business accounts.

Rather than routing every cross-border payment through the SWIFT correspondent banking chain, businesses can now hold balances in multiple currencies within a single account. This means:

- Payments to Philippine suppliers can be made directly in PHP (Philippine Peso) without requiring a full international wire from a GBP account

- USD invoices can be settled from a USD balance held within the same account, avoiding unnecessary GBP-to-USD conversion costs

- Local payment rails in destination countries can be used for final settlement, reducing both cost and settlement time

- Exchange rate exposure can be managed by converting currency at the optimal moment, rather than at the point of payment

According to research published by McKinsey & Company on the future of global payments, the shift toward multi-currency platforms and real-time payment rails is accelerating dramatically, with B2B cross-border payment volumes expected to grow substantially through the decade: https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-the-road-to-nextgen

For UK businesses making regular payments internationally, a multi-currency account is not just a convenience — it is a structural cost reduction.

What UK Businesses Operating in the Philippines Need to Know

The UK–Philippines payment corridor presents a specific set of opportunities and challenges that businesses operating in this space must understand.

The Philippines is one of the most significant remittance-receiving economies in the world, but its financial infrastructure for business-to-business cross-border payments has historically lagged behind consumer channels. Key considerations include:

Regulatory Environment:

- All foreign currency inflows above certain thresholds must be reported to the Bangko Sentral ng Pilipinas

- Beneficiary banks may require additional documentation for inward wires from foreign businesses

- Peso conversion may be subject to local FX market conditions and BSP guidelines

Currency Pair Challenges:

- GBP/PHP is not a highly liquid currency pair on global FX markets

- Most international banks route GBP/PHP via USD as an intermediate currency, adding an additional layer of conversion cost

- This “double conversion” (GBP → USD → PHP) amplifies the FX spread problem described earlier

Practical Implications for UK Businesses:

- Payroll payments to Philippine employees or contractors are subject to local tax withholding obligations (BIR requirements)

- Supplier payments may need to be denominated in USD for practical reasons, even when ultimately converted to PHP by the recipient

- Timing matters: Philippine banking hours and cut-off times are significantly offset from UK hours, which can affect same-day processing

Understanding these nuances is exactly why working with a payments platform that specialises in this corridor — rather than a generic high-street bank — delivers measurable operational and financial advantages.

How PhiliPay Bridges the Gap

PhiliPay was built specifically to serve the needs of UK businesses and individuals with financial ties to the Philippines — and by extension, the broader challenge of managing global payment solutions from a UK base.

Rather than forcing businesses to choose between the limitations of domestic transfers and the high costs of traditional international wires, PhiliPay offers an approach grounded in four principles:

🔒 Secure Every transaction is processed under UK regulatory standards, with robust KYC, AML screening, and data protection protocols in place. For complete details on how your data and funds are protected, you can review the PhiliPay Safeguarding Policy and Privacy Policy.

📊 Transparent No hidden fees. No undisclosed FX margins. What you see is what you pay — a stark contrast to the opaque fee structures of correspondent banking chains.

⚡ Efficient By leveraging modern payment infrastructure and targeted currency expertise, PhiliPay delivers faster settlement and more competitive exchange rates than traditional bank wire processes for the UK–Philippines corridor.

🌍 Global Yet Local Understanding both the UK financial environment and the specific regulatory and operational nuances of the Philippine market means PhiliPay can offer guidance and service that generic multinational banks simply cannot match.

Whether your business needs to pay contractors in Manila, receive revenue from Philippine clients, manage payroll across borders, or simply reduce the cost of your existing international wire programme, PhiliPay provides the infrastructure and expertise to do it better.

Final Thoughts: Choosing the Right Payment Method for Your Business

The distinction between domestic transfers vs international wires is not merely technical — it is financial. Every time your business sends an international payment through a traditional bank wire without evaluating alternatives, you risk paying more than necessary, waiting longer than required, and exposing your cash flow to avoidable FX volatility.

The businesses that thrive in an increasingly globalised economy are those that treat their payment infrastructure as a strategic asset, not an administrative afterthought. They ask the right questions:

- What is the true all-in cost of each international payment we make?

- Are we using the right payment rail for each corridor we operate in?

- Do we have the compliance documentation in place to avoid delays and rejections?

- Could a multi-currency account reduce our conversion costs and settlement times?

If you’re a UK business with payment needs in the Philippines or across Southeast Asia, the answers to these questions could unlock meaningful cost savings and operational improvements.

Ready to take control of your international payment costs?

Explore how PhiliPay can transform the way your business moves money globally — discover the platform here.

Have specific requirements or want to discuss a bespoke solution for your business? Contact the PhiliPay team today and speak with a specialist who understands your market.

Or, if you’re ready to get started right now — open your PhiliPay business account and start making smarter, faster, more transparent international payments today.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or regulatory advice. Businesses should consult qualified financial and legal advisors regarding their specific payment and compliance obligations.